The debt burden of a governmental entity directly affects its ability to provide current services, as well as its long-term fiscal health. Existence of high levels of government borrowing may:

- Indicate that the government is unable to support current programs with current revenues.

- Force future program reductions, increased taxation or additional borrowing when future resources are needed to repay debt.

- Limit capacity to finance capital assets and grants, and to address projected budget gaps.

The State Ranks Second Highest in the Nation in Outstanding Debt

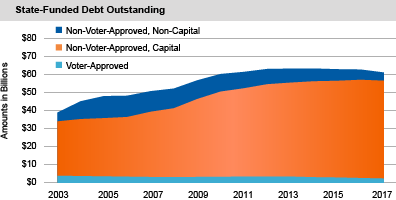

- At the end of SFY 2016-17, the State reported the following categories of debt:

- $2.5 billion in constitutionally recognized (voter-approved) general obligation debt, a decrease of 28.6 percent since SFY 2012-13.

- $49.6 billion in State-Supported debt as statutorily defined in the Debt Reform Act of 2000, a decrease of 5.5 percent since SFY 2012-13.

- $56.2 billion in debt reported in accordance with full accrual accounting under Generally Accepted Accounting Principles (GAAP), a decrease of 2.9 percent since SFY 2012-13.

- $61.4 billion in State-Funded debt, a decrease of 3.3 percent since SFY 2012-13. This category has been defined by the State Comptroller as a comprehensive measurement of the State’s debt burden. It includes instances where the State makes payments with State resources, directly or indirectly, to a public authority, bank trustee or municipal issuer to enable them to make payments on debt issued for State purposes. Approximately 96 percent of State-Funded debt was issued by public authorities without voter approval.

- In 2016, New York State was the second most-indebted state behind California, and fifth among all states in debt per capita.

- At the end of SFY 2016-17, State-Funded debt outstanding per capita was $3,116, which was equal to 5.1 percent of Personal Income.

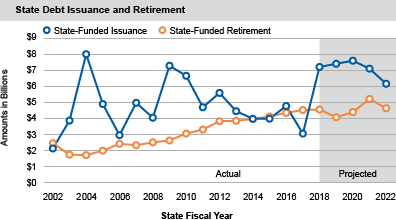

State Projects Issuance of More Debt Than It Will Retire in the Coming Years

- For the next five years, the SFY 2017-18 Enacted Budget Five-Year Capital Program and Financing Plan, as updated in the First Quarterly Update to the SFY 2017-18 Financial Plan, projects that the State will issue 50 percent more debt than it will retire, with:

- $33.7 billion in new State-Supported debt issuance; and

- $20.2 billion in State-Supported debt retirement.

- The State is continuing to experience reduced debt capacity, due in part to the level of debt issued in the past as well as recent economic conditions.

- Based upon scheduled repayment dates, the State’s deficit financing ($2.6 billion at the end of SFY 2016-17) will not be fully repaid until SFY 2025-26. The amount outstanding includes bonds issued by the:

- New York Local Government Assistance Corporation (LGAC);

- Municipal Bond Bank Agency (MBBA); and

- Tobacco Settlement Financing Corporation (TSFC).

- An additional $2 billion in debt outstanding is associated with:

- Issuances by the Sales Tax Asset Receivable Corporation (STARC), which will not be fully repaid until 2034; and

- The sale of Attica Correctional Facility in 1991.

- At times, New York has issued State-Supported debt to fund capital purpose grants to other entities. This practice results in liabilities for the State without creating corresponding State assets.

- In SFY 2016-17, $491 million in State-Supported debt service initially planned for SFY 2017-18 was paid early. With such prepayments, the State sends funds earlier than otherwise planned to the fiscal agent or trustee, who then retains such funds until the regularly scheduled debt service payment is due. Such prepayments do not reduce the State’s interest costs. Prepayments that shift spending from the year in which the payment is due to the prior year deflate reported year-over-year growth in debt service and overall spending.

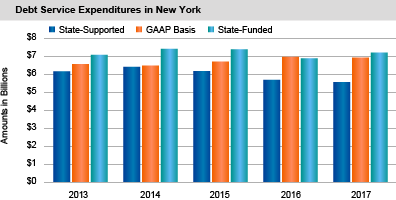

- In SFY 2016-17, State-Funded debt service totaled almost $7.2 billion. This is expected to grow to $8.4 billion by 2022, based on projected issuance and retirement amounts from certain debt issuers in New York State and New York City.

State-Funded Debt Differs from Debt Reported Under GAAP

- Significant differences exist between debt reported under the State-Funded category for cash reporting and debt reported under GAAP:

- State-Funded debt includes certain obligations that are not recognized as a State liability under GAAP, including:

- $1.9 billion in STARC bonds originally issued in fiscal year 2005 that will be repaid from future sales tax revenues of the State; and

- $7.9 billion in Building Aid Revenue bonds issued by New York City’s Transitional Finance Authority (TFA) for education purposes since fiscal year 2007 that will be repaid with pledged local assistance payments from the State.

- State-Funded debt also includes:

- $956 million in obligations for State University of New York dormitory facilities paid with rental fees assigned to the Dormitory Authority and reported as collateralized borrowing under GAAP; and

- $157 million for certain contingent-contractual obligations associated with the Secured Hospital Program reported as accrued liabilities under GAAP.*

- Debt reported under GAAP but not counted in the State-Funded debt measurement includes:

- $4.9 billion in bond premiums;

- $13 million in accumulated accretion on capital appreciation bonds; and

- $542 million in certain vendor-financed capital lease obligations and mortgage loan commitments.

- State-Funded debt includes certain obligations that are not recognized as a State liability under GAAP, including:

State’s Bond Ratings

- At the end of SFY 2016-17, the State’s general obligation bond ratings were assigned as follows:

- AA+ by Fitch Ratings;

- AA+ by Kroll Bond Rating Agency, Inc.;

- Aa1 by Moody’s Investors Service; and

- AA+ by Standard & Poor’s (S&P) Rating Services.

These ratings are one step below the highest investment grade ratings.

*In SFY 2013-14, the State was called on to make approximately $12 million in payments on certain contingent-contractual bonds from the Secured Hospital Program that was enacted in 1985 in which the State issued bonds for certain distressed hospitals. The required payment has increased to nearly $30 million in SFY 2016-17. As of March 31, 2017, the Secured Hospital Program included contingent-contractual debt obligations totaling approximately $220 million, including $157 million related to certain distressed hospitals where the State has previously been called on to make debt service payments.