The Tourism Industry in New York City

Reigniting the Return

April 2021

Highlights

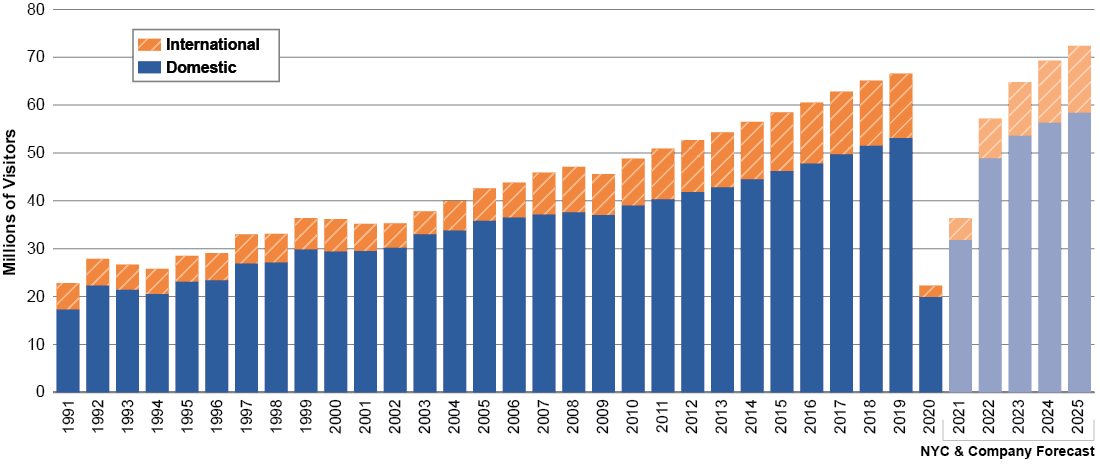

- In 2020, the 10-year period of record growth in tourism came to an end, and the number of visitors to New York City fell by 67 percent to 22.3 million (from 66.6 million in 2019).

- OSC estimates the industry’s economic impact dropped by 75 percent from $80.3 billion in 2019 to $20.2 billion in 2020.

- Employment in the tourism industry declined by 89,000 jobs (31.4 percent) to 194,200 in 2020, from a record 283,200 jobs in 2019.

- Tourism accounts for 7.2 percent of total private sector employment and 4.5 percent of private sector wages. Tourism indirectly supported 376,800 jobs in 2019.

- In 2019, leisure travelers accounted for 80 percent of visitors, while domestic travelers also made up 80 percent of visitors to New York City. However, business and international travelers have higher average spending per visit.

- The industry supports a higher share of workers who are self-employed (14.4 percent), low-wage ($32,000 annually), minority (66 percent), and immigrants (44.7 percent) and most (60 percent) do not have a bachelor’s degree.

- In 2019, the number of tourists visiting New York City had almost tripled in the 28 years since 1991, with almost half the growth occurring in the past 10 years.

- The hotel industry in Manhattan, which has the highest wages and the third-highest industry employment of any county in the nation, was impacted severely, losing 46 percent of its jobs in 2020.

- Tourism-related tax revenue accounts for 59 percent of the City’s $2 billion decline in tax collections, or about $1.2 billion, for FY 2021.

New York City is a top global destination for visitors drawn to its museums, entertainment, restaurants and commerce. The City is also host to conventions and trade shows, and major athletic events such as the New York City Marathon and the U.S. Open.

The tourism industry is a vital component of New York City’s economy, supporting more than 376,800 jobs (representing nearly 10 percent of all private sector employment). The industry functions as a dynamic ecosystem of attractions — shows, events, shopping and food — glued together by hospitality and transport, which serve as the core infrastructure.

Visitors and visitor spending are the essential factors in measuring the health of the industry. After reaching a record high of 66.6 million visitors in 2019 and generating $47.4 billion in spending, the number of visitors to New York City dropped by 67 percent and their spending declined by 73 percent in 2020. The Office of the State Comptroller (OSC) estimates the drop in spending cost the City $1.2 billion in lost tax revenues.

The industry experienced strong growth in employment and wages in the decade preceding 2020. OSC estimates the industry lost nearly a third of its employment in 2020. Visitors and their spending are not projected to reach pre-pandemic levels before 2025. Employment is unlikely to rebound fully before visitor spending.

In its effort to reignite the tourism industry, the City cannot simply rely on vaccinations and reopening — which are necessary steps — for the industry to return, but must also develop a proactive strategy that cultivates and attracts international and business travelers to restore the industry to robust health and return to a path of continuous and shared growth.

Visitors and Spending Profile

According to NYC & Company, the City’s tourism agency, a tourist is defined as any person (foreign or domestic) who travels at least 50 miles to visit the City, or lodges there for one night either for business or leisure. This report uses the terms “visitor” and “tourist” interchangeably.

Visitor Characteristics

New York City hosted 66.6 million visitors in 2019 (about 25 percent of the State’s 265.5 million visitors that year), a tenth-consecutive annual record. In 2020, the pandemic and related behavioral and governmental restrictions caused the number to drop to 22.3 million, a 67 percent reduction (see Figure 1).

FIGURE 1 – Total Visitors to New York City

Sources: NYC & Company; OSC analysis

Since 1991, the number of visitors to the City has nearly tripled, with almost half the growth occurring in the last 10 years (2009 to 2019). New York City’s consistent ranking as a top 10 destination city globally and actions facilitating and promoting tourism have helped support this growth.1

Total visitor spending in the City was $47.4 billion and accounted for 64.4 percent of the State’s total visitor spending of $73.6 billion, while the City accounted for 25.1 percent of the State’s 265.5 million tourists.

International

International tourism has risen steadily over the decades; however, it is only over the past decade that it became the primary driver of visitor growth. From 2009 to 2019, international tourism grew at a considerably faster pace than domestic. Prior to 2009, when Congress established a public-private entity to promote tourism (Brand USA), the annual growth in domestic visitors was higher than in international tourists.

While the majority of visitors to New York City are domestic, international visitors have a greater impact per visitor on the City’s economy. Generally, the economic value (i.e., the spending) of one international visitor is equivalent to that of four domestic tourists. In 2019, the average spending by an international visitor was $1,709 compared to $458 per domestic traveler.

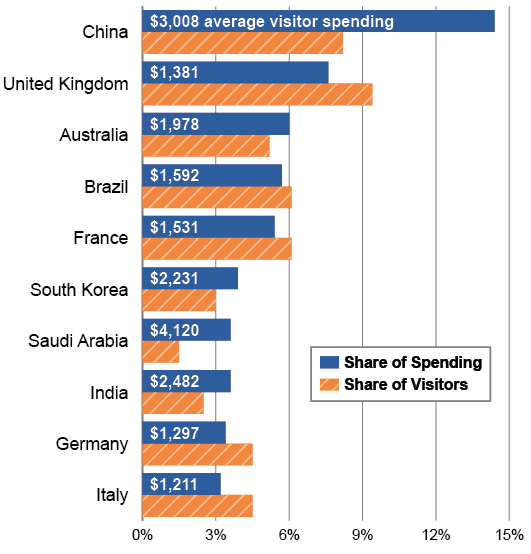

International visitors to the City generally spend about twice the amount per visit compared to the average international traveler to the U.S., based on data from Tourism Economics, a global travel and tourism econometric firm. International visitors who account for the highest shares of spending are shown by country of origin in Figure 2. Visitors from China have posted record visitor spending for three years in a row (2017-2019). In 2019, spending by these visitors totaled $3.3 billion. Each Chinese tourist spent an average of $3,000, almost 60 percent higher than the average for international visitors. From 2009 to 2019, tourists from China increased more than sevenfold, the strongest growth of any nation.2 The U.S. Department of Commerce agreement with China in December 2007 to facilitate more group leisure travel helped accelerate visitor growth. The share of international visitors from China to the U.S. more than quadrupled from 2007 to 2018.

FIGURE 2 – Share of Total International Spending and Visitors by Country of Origin, 2019

Note: Chart data displays top 10 countries by spending.

Sources: NYC & Company; OSC analysis

The United Kingdom (with average tourist spending of $1,381) has historically been the top foreign source of visitors to the City.3 Currency exchange rates have played a significant role in the U.K.’s impact on the City economy. Prior to 2017, the highest visitor spending in any year by one country was from the United Kingdom in 2008 ($2.3 billion), primarily due to the strong exchange rate (about $2 per British pound). While Canada typically accounts for the second-highest number of visitors to the City, its share of total visitor spending ranks at the lower end (2 percent), with an average amount of $476. Among international visitors, Canadian tourists are expected to return soonest, in 2023.

Many factors affect international tourism, including foreign visitor protocols (visa processing and waiver programs) and trade agreements. Cost (travel affordability and currency exchange rates), safety and ease of travel are critical factors as more than four out of five international travelers visit the City for leisure purposes. Figure 3 shows the share of business and leisure travelers by origin.

FIGURE 3 – Share of Visitors by Category (2018–2019)

| Category | Share of Domestic | Share of International | Share of Total |

| Business | 22% | 17% | 20% |

| Leisure | 78% | 83% | 80% |

Sources: NYC & Company; OSC analysis

Domestic

Since 1991, domestic visitors to the City have more than tripled. However, the strongest decade of growth for domestic tourism was during the 1990s, when growth averaged about 7 percent per year. In the most recent 10-year period prior to the pandemic, domestic growth had been cut in half. Spending by domestic visitors totaled $24.3 billion in 2019, or nearly 51.3 percent of total visitor spending, and declined to $8.2 billion (down 66 percent) in 2020.4

Almost two-thirds of domestic visitors to the City come from the rest of New York State, and (in order of visitor share) New Jersey, Pennsylvania, Connecticut and Massachusetts. The average spending is $492 per person per trip. For most of 2020, travelers from contiguous states were exempt from quarantine requirements. In early April 2021, quarantine rules were lifted for all domestic and international visitors.

Leisure

Leisure travelers on average account for 79 percent of visitors to the City and 71 percent of visitor spending. In recent years (prior to the pandemic), the growth in leisure travelers has been slowing.

Slightly more than half of domestic leisure visitors are “day-trippers” who do not stay overnight, while the remaining portion that stay in a hotel have an average stay of two days. Visiting friends and family is the primary motivation for a third of these travelers. The top five domestic leisure visitor activities include dining, shopping, museums, theaters and nightlife.

International leisure travelers are more likely than their domestic counterparts to stay in a hotel (76 percent), and primarily visit the City as a vacation destination. These travelers typically plan their trips about four months in advance of arrival. Their top five activities include sightseeing, shopping, museums, monuments and historical locations.

Business

Business travelers account for 20 percent of all visitors to the City, and the annual growth in business travel had remained fairly steady prior to the pandemic.

More than 80 percent of business travelers are domestic, and almost three out of four stay in a hotel, with an average duration of about two days. The mix between transient and group travel (i.e., conferences, conventions) is fairly even.5 The top three activities for domestic business visitors include dining, nightlife and museums.

International business travelers are more likely to stay in a hotel and for a longer duration (nearly a week). A majority of international business travelers come to the City for transient business, while more than a third arrive for conferences or conventions. The top three activities include shopping, sightseeing and museums.

Business travelers spend more on average than leisure visitors. Domestic business visitors spend an average of $860 per person, more than twice the spending of domestic leisure tourists. International business travelers spend nearly $2,000 per person, which is 30 percent more than international leisure travelers.

Meeting and convention delegate travel averaged about 6.2 million visitors, about half the number of business travelers, between 2016 and 2018.6 These conventioneers attend events and programs at the Javits Center, Piers 92 & 94, major hotels and other venues across the City. International convention delegates spend 2.6 times more than their domestic counterparts ($1,853 compared to $726).

Importance of Visitor Spending

Spending by tourists is the critical driver for industry employment, wages and tax revenues. Tourism Economics forecasts that visitor spending will return to pre-pandemic levels in five years (2025), whereas it took three years to rebound after the financial crisis in 2008.

Visitor spending spans several sectors, from hotels, restaurants and retail shops to Broadway shows, concerts and sightseeing venues. Spending also includes taxicabs, buses and limousine services. Figure 4 breaks down visitor spending by category.

FIGURE 4 – Visitor Spending by Category, 2019

| Spending Category | Visitor Spending (billions) | Share of Total |

| Lodging | $13.5 | 28.2% |

| Food and Beverage | $10.5 | 21.9% |

| Retail | $9.3 | 19.4% |

| Arts, Culture & Entertainment | $5.6 | 11.7% |

| Local Transportation | $8.5 | 17.7% |

| Miscellaneous | $0.5 | 1.0% |

| Total | $47.9 | 100.0% |

Note: The total is higher than the $47.4 billion reported due to rounding.

Sources: NYC & Company; OSC analysis

More than half of visitor spending (53 percent) is targeted to restaurants, shopping, and arts, culture and entertainment. Prior OSC reports have addressed the impact of the pandemic on the restaurant, retail, and arts, entertainment and recreation sectors.7 Most of visitors’ remaining spending (46 percent) is on hotels and transportation, which are areas of focus in this report.

Industry Profile

From an industry classification standpoint, the tourism industry spans the broader leisure and hospitality, transportation, and retail sectors, but it does not fully encapsulate these sectors because the largest patrons of retail stores and restaurants are local residents. Tourism does fully impact certain subsectors, however, such as hotels, air travel, sightseeing, promoters and cultural venues. Appendix A provides detail on OSC’s tourism industry definition and respective industry weights, which build on prior analysis from the New York State Department of Labor.8

Employment

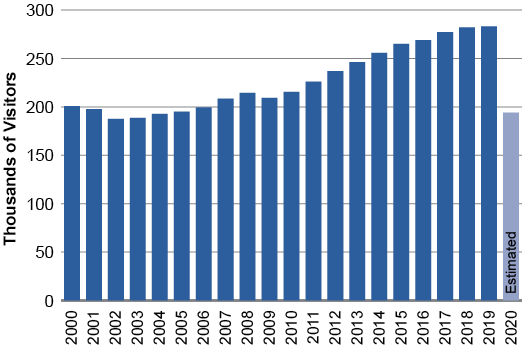

The tourism industry, as defined by OSC, employed a record 283,200 workers, accounting for 7.2 percent of private sector jobs and 4.5 percent of wages in 2019. This reflected a 35 percent increase from 2009 levels, faster than the growth in total private sector jobs (30 percent). OSC estimates that in 2020, employment fell to 194,200, reflecting a drop of 31.4 percent (or 89,000 jobs), the lowest level since 2004 (see Figure 5). The City’s tourism industry represented 53.5 percent of the State’s total tourism employment in 2019.

FIGURE 5 – Tourism Employment in New York City

Sources: NYS Department of Labor, QCEW; OSC analysis

Employment in tourism is primarily concentrated in three large sectors: leisure and hospitality (59 percent of tourism jobs); retail (19.3 percent); and transportation (16.1 percent). The top three subsectors (hotels, restaurants and air transportation) account for almost 41 percent of all tourism industry employment (see Figure 6).

FIGURE 6 – Top Three Subsector Shares of Tourism Jobs

| Subsector Description | Jobs | Share of Tourism Jobs |

| Hotels (except casino hotels) and Motels | 51,342 | 18.1% |

| Full Service Restaurants | 33,288 | 11.8% |

| Scheduled Passenger Air Transportation | 30,979 | 10.9% |

Note: Subsectors are defined by North American Industry Classification System (NAICS) created by the Census Bureau.

Sources: NYS Department of Labor; OSC analysis

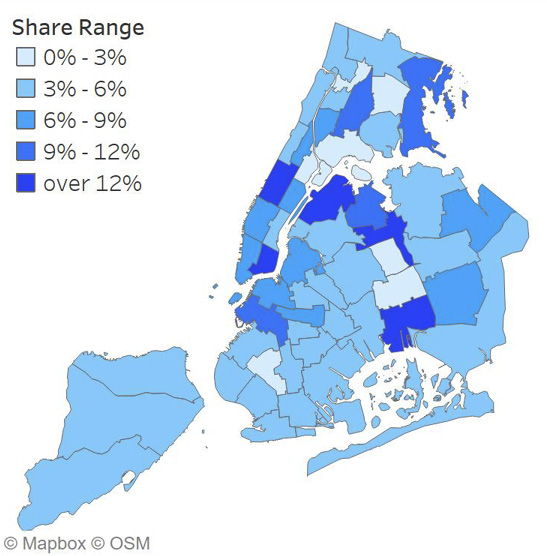

The majority of the City’s tourism jobs (57.6 percent) are located in Manhattan. The Chelsea, Clinton & Midtown area has the most jobs related to tourism, exceeding 81,000, or 7.8 percent of all employment in the neighborhood. Tourism employment in Chelsea was concentrated in hotels (31.7 percent of total), performing arts promoters (11.7 percent) and full-service restaurants (11.1 percent). Of the 10 neighborhoods with the most tourism jobs, six were located in Manhattan, underscoring the concentration of tourism activity there.

The second-highest concentration is in Queens, with 24 percent of tourism employment. The Astoria & Long Island City area had the highest share of total employment in tourism-related industries, at 19.0 percent. This was driven by employment in scheduled air passenger transportation (67.2 percent of total; see Figure 7).

FIGURE 7 – Tourism Share of Employment by Neighborhood

Sources: NYS Department of Labor; OSC analysis

Work Force Characteristics

Overview of Employees in Tourism:

- Most are NYC residents (83%)

- Higher share are self-employed

- 14.4% vs. 8.5% City average

- Lower median wage ($32,000) than City ($50,000)

- Almost a third are part-time workers

- 31.9% vs. 23.6% City average

- Generally younger: 41% under the age of 35

- 60% do not have a bachelor’s degree

- Nearly two-thirds are minorities

- Higher share of immigrants

- 44.7% vs 41.1% City average

- Over 80% come from Latin America or Asia

In 2019, according to the Census Bureau, 385,000 workers declared their main source of income was from the City’s tourism industry, and most (82.6 percent) were City residents. In addition to those employed by private companies and the government, these workers include self-employed people. Self-employed workers made up 14.4 percent of the tourism work force in 2019, much higher than the 8.5 percent share of self-employed people in the City’s total work force.

Workers in the tourism industry earn lower salaries than the citywide work force. In 2019, the median wage in the tourism industry was just $32,000, lower than the City’s overall median of $50,000. Less than a third of tourism workers earned more than $50,000. One factor contributing to the lower wage is that almost one-third (31.7 percent) of tourism employees are part-time workers (i.e., worked less than 35 hours per week and/or worked less than 50 weeks per year), much higher than the share of part-timers (23.6 percent) in the City overall.

Workers in the tourism industry are also younger than the City’s work force overall. The average age of tourism workers was 40.4 years, lower than the average age of 41.9 in the City work force. Also, 40.9 percent of the tourism work force was younger than 35, a higher share than in the total work force (35.8 percent).

Workers in the tourism industry hold a variety of occupations. Taxi drivers were the only group that exceeded 5 percent of employment (see Figure 8). Of the top 15 occupations in the industry, all but one (Other Managers) do not need a bachelor’s degree for entry, according to the Bureau of Labor Statistics. This may be why 60 percent of the work force who are age 25 and older do not have a bachelor’s degree, a higher share than among the City’s total work force (48 percent).

Almost two-thirds (66.2 percent) of the tourism work force is composed of minorities, a higher share than the 60.8 percent among the citywide work force. Among tourism workers, 27 percent were Hispanics or Latino, 18 percent were Black or African American, and 17 percent were Asian American.

Tourism workers are also more likely to be immigrants, making up 45.5 percent of the industry, compared to 41.1 percent in the total work force. More than four-fifths (81.2 percent) of the immigrant workers in tourism came from Latin America or Asia.

FIGURE 8 – Top 15 Occupations in Tourism, 2019

| Occupation | Share of Sector | Average Wage |

| Taxi Drivers | 7.8% | $19,600 |

| Cashiers | 4.5% | $23,200 |

| Maids and Housekeeping Cleaners | 4.3% | $42,700 |

| Waiters and Waitresses | 3.3% | $29,300 |

| Retail Salespersons | 3.2% | $39,200 |

| Other Managers | 3.1% | $76,400 |

| First-Line Supervisors of Retail Sales Workers | 2.7% | $53,800 |

| Janitors and Building Cleaners | 2.6% | $34,100 |

| Customer Service Representatives | 2.5% | $36,000 |

| Cooks | 2.5% | $28,300 |

| Exercise Trainers and Group Fitness Instructors | 2.0% | $51,800 |

| Driver/Sales Workers and Truck Drivers | 1.9% | $32,500 |

| Flight Attendants | 1.8% | $50,500 |

| Chefs and Head Cooks | 1.5% | $38,500 |

| Food Preparation Workers | 1.5% | $25,400 |

| Subtotal | 45.2% | $36,500 |

Sources: U.S. Census Bureau, American Community Survey, 2019 1-year survey; OSC analysis

Firms

There are 60,800 firms in New York City that provide at least some of their services in support of tourism. Of these, 39.5 percent are located in Manhattan, while Brooklyn and Queens also account for large portions (25.3 percent and 22.5 percent, respectively). The tourism industry has a bigger share of large firms (greater than 10 employees) than the private sector as a whole, given that the three largest subsectors are hotels, full service restaurants and air transportation.

Wages and Average Salaries

Just as tourism employment grew faster than the City’s total private employment in the past decade, the growth in wages in the tourism industry also outpaced total private wages. In the 10 years before the pandemic, total wages in tourism increased by 81.7 percent to reach $17.1 billion in 2019, while citywide private wages increased by 64.3 percent.

The average annual salary in the tourism industry was $60,400 in 2019, lower than the City’s total average private sector salary of $97,700. Much of the tourism industry includes lower-paying subsectors. The largest, accommodation and food services, has an average annual salary of $49,800. The second-largest, retail trade, had an even lower average at $41,200. The average salary across all of the tourism sector is lifted by the transportation and the arts and recreation subsectors, with average salaries of $74,600 and $90,600, respectively. The arts, entertainment and recreation sector has a higher average salary but a relatively small number of workers9 (see Figure 9).

FIGURE 9 – New York City Tourism Sector – Average Annual Salaries in 2019

| Occupation | Average Salary | Share of Tourism Wages |

| Accommodation and Food | $49,800 | 34% |

| Arts, Entertainment and Recreation | $90,600 | 28% |

| Retail | $41,200 | 13% |

| Transportation | $74,600 | 20% |

| Other | $62,100 | 5% |

| Total | $60,400 | 100% |

Sources: NYS Department of Labor; OSC analysis

Tourism’s average salary has increased by 34.3 percent since 2009, faster than the total private sector average (26.6 percent). The growth was boosted by the increase in New York State’s minimum hourly wage to $15, which began to be phased in beginning in 2016 and was fully implemented in 2018 for large employers (11 or more employees) and by 2019 for small employers. There are slightly lower wage minimums for tipped workers (i.e., employers can satisfy the wage requirement for food service workers by combining a cash wage of $10 per hour with a tip allowance of no more than $5). Many occupations in the tourism industry pay the minimum wage, as these jobs generally do not require a high level of educational attainment or work experience.

Industry Focus

As stated earlier, OSC has published a series of reports highlighting the impact of COVID-19 on different sectors of the City’s economy. Prior reports have focused on the retail, restaurants and arts, entertainment and recreation sectors, which are all a part of the tourism ecosystem. Discussed below are the two large remaining sectors: hotels and accommodations, and transportation.

Hotels and Accommodations

The hotel and accommodations sector provided 52,000 jobs and $3.6 billion in wages in 2019, and included 883 firms.10 As a share of the tourism industry, it represents 18.4 percent of employment, 21.1 percent of wages and 4.8 percent of firms. In 2020, this sector lost nearly half of its employment base (23,813 jobs or 44 percent).

Hotels and motels, except casino hotels (see Appendix A), account for almost all the jobs and wages for this sector. Hotels and motels employment dropped by 46 percent in 2020, and nearly all the jobs (88 percent) and wages (93 percent) are in Manhattan. In 2019, Manhattan had the highest total annual wages for hotels and motels out of all U.S. counties, totaling $3.3 billion, or 68 percent more than the second-highest (Los Angeles County, at $1.97 billion). Manhattan was third in employment, after Orange County (in Florida) and Los Angeles County.

Prior to the pandemic, factors that affected the hotel industry were: oversupply, which pressured average daily rates; high construction costs; and increased competition from online lodging marketplaces such as Airbnb. Since OSC’s prior report on the hotel industry, the supply of rooms in the City has increased by 20 percent (from 2015 to 2020).11

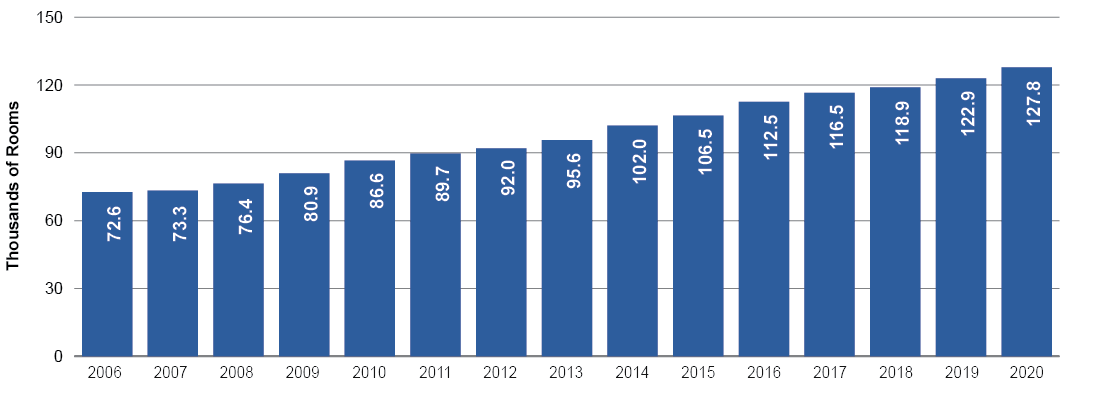

According to a 2020 Department of City Planning report (NYC Hotel Market Analysis), New York City had a total of 705 hotels with a total of 127,810 rooms in January 2020. By September 2020, 20 percent of the hotels and 31 percent of the rooms were shut down. Of the rooms that were closed, 9 percent were closed permanently. Manhattan accounted for nearly all of the room closures in the City. As of October 2020, more than 37,000 hotel rooms in the City remained closed, with 10 percent permanently shut down (see Figure 10).

FIGURE 10 – Hotel Rooms in New York City

Source: NYC & Company; 2020 data is from Department of City Planning Report

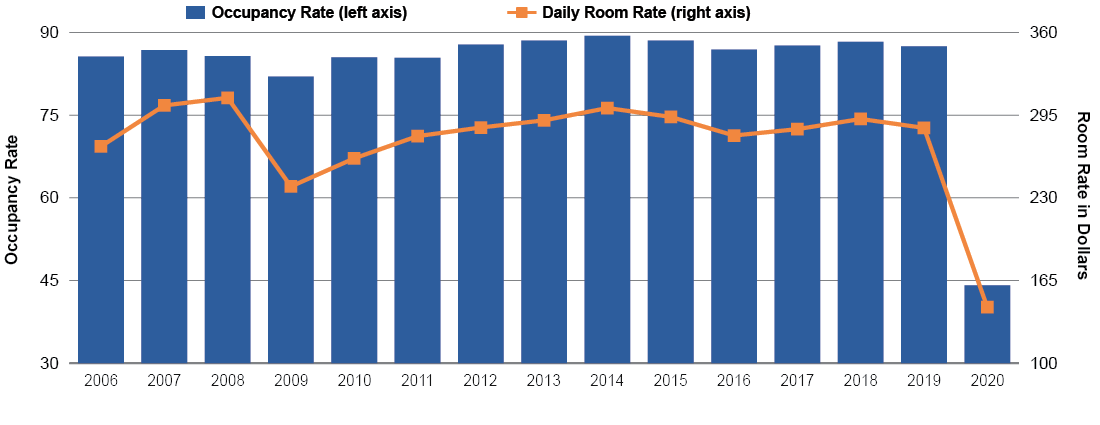

Prior to the pandemic (September 2019), hotel occupancy in the City was 89.6 percent, the highest in the nation, and was a key factor attracting hotel builders and operators. By September 2020, occupancy had dropped to 38.9 percent, pressuring daily room rates. NYC & Company estimates hotel occupancy in 2020 was half of pre-pandemic levels (see Figure 11). However, most of the occupancy was supported by contracts to house homeless people, airline crews, health care workers and people requiring quarantine. As of October 2020, the City had spent $893 million in COVID-19-related contracts for hotels, representing 20 percent of its total pandemic-related contracts.

FIGURE 11 – Manhattan Hotel Rooms

Sources: CBRE Hotels; NYC & Company; OSC analysis

At the end of 2020, there were 17,800 homeless people living in hotels throughout the City, compared to 11,500 at the end of 2019. The number of single-adult homeless individuals sheltered in hotels in 2020 increased by 9,341. Excluding government contracts, the occupancy rate attributable to tourists in 2020 was as low as 10 percent. Prior to the pandemic, 9 percent of all hotel rooms in the City were housing homeless people, not including essential and health care workers, and this increased to nearly 20 percent by the end of the year.

Given the forecast that between 10 percent and 25 percent of closed hotel rooms will remain permanently shut, the overall supply of rooms available for tourists (excluding homeless services and government contracts) is expected to decline by about 19 percent (24,600 rooms), though not for long. According to Lodging Econometrics, 150 hotels (25,640 rooms) are in the new construction pipeline, with 108 hotels currently under construction. In 2020, nine new hotels opened in the New York City market. Development did not decline significantly in 2020, as projects were delayed rather than canceled. The expectation is that travel will resume, and that building a hotel in a downturn represents a unique and potentially valuable opportunity for owners.

Revenue per average room (RevPAR), which is a performance measure calculated by multiplying the average daily room (ADR) rate by the occupancy rate, declined by about 75 percent in 2020. Manhattan’s occupancy and ADR rates drive the City’s RevPAR.

According to the Department of City Planning report, demand for hotel rooms in New York City is not expected to fully recover to pre-pandemic levels until 2025, around the time tourism is expected to recover; demand in the U.S. is expected to recover earlier, by 2023. According to STR, a global hospitality industry consultant, through the third week of March, occupancy in City hotels had climbed to slightly over 50 percent.

Airbnb

Apart from traditional hotel rooms, the short-term rental market, dominated by the likes of Airbnb in New York City, have created a type of shadow hotel market. There are about 50,000 Airbnb listings in the City (its largest U.S. market), equivalent to almost 40 percent of the hotel room inventory. Short-term rental market listings declined 11 percent through September 2020. More than 80 percent of total short-term rental listings before and during the pandemic were in Manhattan and Brooklyn. Prior to the pandemic, concerns had grown over the supply created by these rentals and their impact on ADR, as well as their payment of required hotel taxes and fees.

Transportation Sector

The private transportation sector is a significant component of overall tourism employment, as tourists need to travel both to and within the City. Private tourism-related transportation employment totaled 45,700 jobs in 2019 and declined by 20.9 percent in 2020. Transportation employment represents 16.1 percent of total tourism jobs and almost 20 percent of wages.12

Air transportation and related services, including airport operations, account for more than 84 percent of total tourism-related transportation jobs, and this subsector has a comparatively higher average salary of $80,200. Scenic and sightseeing transportation, along with taxi and limousine services, each account for less than 5 percent of tourism-related transportation employment, and their average salaries are about half that of the air transport sector.

Air

Air transportation has been impacted by the sharp drop in passenger numbers and in the number of flights arriving and departing, which were down 69.1 percent in City-area airports in January 2021. OAG, an air travel analytics firm, estimates that the number of active air routes globally in late February were down 28.2 percent compared to the prior year. Fewer options for air travelers represent another barrier to recovery in tourism activity. While OAG reports that airlines have begun increasing capacity, and it expects the trend to strengthen through the spring and summer, the industry may have to contend with other challenges, including the potential of a commercial pilot shortage. More than three-fourths of international leisure visitors (78 percent) use the City as a port of entry to the United States, underlining the importance of the City’s transportation sector.

Taxi

Yellow taxis primarily rely on fares that originate on Manhattan streets (hails) and at airports; the reduction in visitors has had an outsized impact on their business. According to the City’s Taxi and Limousine Commission, the average trips per day declined by 96 percent from January 2020 to its trough in April 2020. The daily farebox totals for yellow and green cabs were down 79.5 percent in January compared to the prior year. City taxis require an official medallion to operate, and drivers often take on significant debt in order to obtain them. This has led to a debt crisis among taxi drivers that has been exacerbated by the pandemic. Mayor de Blasio has proposed a medallion relief plan, but the New York Taxi Workers Alliance has called the plan insufficient.

Prior to the pandemic, taxicab drivers had been facing a challenging competitive landscape due to the advent of ride-sharing firms such as Uber and Lyft. According to the Taxi and Limousine Commission 2020 Annual Report, there were more than 75,000 high-volume for-hire service vehicles (i.e., ride-hailing apps) in the City, compared to 13,587 medallion taxi vehicles. In 2019, the average yellow cab trips per day were down about 42 percent from 2015, while ride-hailing apps experienced a sixfold increase over the same period.13 The average daily farebox (excluding tips) for yellow cabs declined by one-third over the same period. In 2018, the City capped the number of app-based for-hire cars and established a minimum pay schedule.

Pandemic Impact

As the COVID-19 pandemic began to spread in the spring of 2020, the number of travelers passing through the country’s airports fell dramatically. By the middle of April 2020, passenger traffic had declined by about 96 percent. A similar trend occurred in City-area airports (e.g., JFK, LaGuardia, Newark and Stewart). However, as national air passenger volumes slowly increased over the spring and summer, New York City volumes lagged. In August 2020, air passenger screenings were down 71.0 percent in the nation and 80.6 percent in New York City. Despite some improvement over the fall and winter, the City still lags the nation, and the number of passengers screened in February 2021 remained well below prior-year levels, down 59.5 percent and 70.1 percent, respectively, in the nation and the City.

As Figure 12 shows, the drop in visitor spending was more severe than the decline in the number of visitors due to the sharp drop in international tourists. Tourism spending declined by nearly 73 percent in 2020, driven by a sharp drop in international spending.

FIGURE 12 – Pre- and Post-Pandemic Share of Visitors and Spending Breakdown

| Category | Visitors 2019 (millions) | Visitors 2020 (millions) | Spending 2019 (billions) | Spending 2020 (billions) |

| Domestic | 53.1 | 19.9 | $24.3 | $8.2* |

| International | 13.5 | 2.4 | $23.1 | $4.7* |

| Total | 66.6 | 22.3 | $47.4 | $13.0* |

| Percentage Change: 2020 vs. 2019 | (67%) | (73%) | ||

*Denotes OSC estimates

Sources: NYC & Company; Tourism Economics; OSC analysis

In 2020, international tourism declined by 82 percent, more than the 61 percent decline in domestic visitors. In both the previous economic downturns (in 2001 and 2008), international visitors dropped off more severely than domestic tourists. According to NYC & Company, the rebound in 2021 is off to a slower start than anticipated with much of the growth forecasted for the second half of the year.

The most substantial federal relief program to aid businesses was the Paycheck Protection Program. In 2020, the Paycheck Protection Program (PPP) granted loans to 42,800 City businesses in tourism-related industries, for a total value of $3.4 billion. These businesses accounted for 27 percent of PPP loans in the City, and 18.3 percent of loan dollars disbursed. Loans were concentrated in restaurants (27.7 percent of the loan dollars granted to tourism-related industries) and hotels (11.7 percent).14 Significant standalone federal grants programs have also been created for restaurants and entertainment venues, which should encourage reopening and expansion of operations, and attract visitors back to the City.

Economic Impact

While the number of visitors is a frequently cited measure, the critical factor for gauging the strength of the tourism sector is visitor spending, which directly impacts economic activity and tax revenues.

OSC estimates (utilizing the IMPLAN® model and inputs provided by OSC) that the tourism industry in New York State generated a record economic impact of nearly $75.3 billion in 2019. While tourism is big business throughout the State, the greatest economic impact was in New York City totaling $51.7 billion, which accounts for more than two-thirds of the State’s impact. Including indirect and induced effects, the impact on the City would be $80.3 billion in support of 376,800 jobs.15

Based on OSC’s estimate of $13.0 billion in total visitor spending for 2020 and applying the value-added multiplier generated from IMPLAN of 1.55, the total economic impact declined to $20.2 billion, a 75 percent reduction from 2019 levels.

The U.S. Bureau of Economic Analysis reports the breakdown of gross domestic product by county, which can be used to calculate the impact of tourism on the City’s economy. In 2019, tourism was responsible for 3.5 percent of the City’s gross product, higher than its national share (2.9 percent) of gross domestic product.16

Among the five boroughs, Queens had the highest share of its gross product driven by tourism (7.2 percent), as both JFK and LaGuardia airports are located there. In Manhattan, only 2.9 percent of the gross product was the result of tourism, as it is home to several high-output sectors (such as the securities industry), which contribute an outsize share of the borough’s gross product.

According to the 2019 Javits Center Annual Report, more than 2 million attendees to the center’s shows and events in 2018 generated over $1.9 billion in sales activity and more than $88 million in City taxes, plus an additional $4.1 million for the MTA. Since spring 2020, the Javits Center has been repurposed for activities related to the pandemic response.

Tax Revenue Impact

OSC estimates that in City Fiscal Year (FY) 2020, ending June 30, 2020, the tourism industry generated $5.3 billion in tax revenues for the City, representing 8.3 percent of total tax collections. For FY 2021, ending June 30, 2021, OSC forecasts tourism-related tax revenue to decline by $1.2 billion to $4.1 billion (see Figure 13). This shortfall accounts for 59 percent of the City’s projected $2 billion decline in tax collections for FY 2021 (to $61.1 billion from $63.1 billion in FY 2020).

FIGURE 13 – Tourism Tax Revenue by Category

| Tax Category | FY 2020 | FY 2021 | Annual Change | Share FY 20 | Share FY 21 |

| Property | 2,333 | 2,509 | 8% | 45% | 63% |

| Sales | 1,300 | 612 | -53% | 25% | 15% |

| Personal Income | 618 | 365 | -41% | 12% | 9% |

| Hotel | 468 | 75 | -84% | 9% | 2% |

| Business | 493 | 445 | -10% | 8% | 10% |

| Real Estate Transaction | 45 | 52 | 16% | 1% | 1% |

| Total | 5,257 | 4,058 | -23% | 100% | 100% |

Sources: NYC Office of Management and Budget; OSC analysis

In the current fiscal year, nearly half the decline in tourism tax revenues is due to a sharp drop in sales tax collections from $1.3 billion in FY 2020 to $612 million FY 2021. Hotel taxes, which are based on occupancy levels, will feel the greatest impact, declining by 84 percent in FY 2021 to $75 million.

Property taxes, which represent the largest portion of tourism tax revenues, are expected to rise in the current fiscal year, as they are based on assessments from the prior year. However, the lagged impact of the pandemic is expected to reduce property tax revenue by $430 million in FY 2022 based on the decline in market valuations for hotels, retail and other tourism-related properties.17 If tourism-dependent properties are unable to pay property taxes, this could further deteriorate tax revenues from the industry. The hotel tax delinquency rate at the end of March reached a record 6.7 percent, a significant increase from the below 1 percent average over its recent history (prior peak was in FY 2011 at 2.1 percent).

Outlook for Tourism

The COVID-19 pandemic presents different — and potentially more long-term — behavioral changes than the previous downturns in 2001 and 2008 (both of which were initiated by tightening monetary policy, and one of which was impacted by a terrorist attack). The pandemic brings many more variables into play, such as herd immunity, vaccination availability and acceptance, and changes in professional and social interactions (including the accelerated use of technology-facilitated communications). Furthermore, the impact on tourism-related industries specifically has been unprecedented, and a return to pre-pandemic activity will likely take longer than it has in prior downturns.

NYC & Company forecasts that domestic leisure travelers (primarily those making day trips) will be the first to rebound to 2019 levels, as they face the fewest obstacles from an infrastructure and mobility standpoint. International travelers, who have a higher per-visitor economic impact, are not expected to return to pre-pandemic levels before 2025.

NYC & Company forecasts that the total number of visitors will return to pre-pandemic levels by 2024, with a full recovery including international travelers to occur by 2025. The Office of Management and Budget, however, is more optimistic, and believes this will occur much earlier.

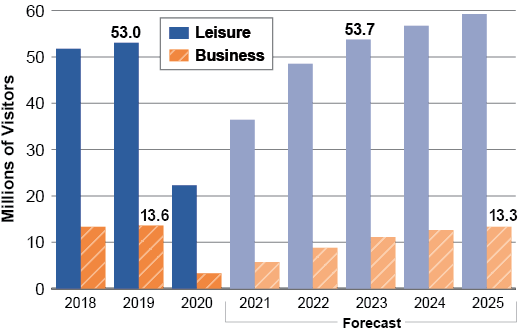

Business travelers to the City are not projected to surpass 2019 levels for the foreseeable future, according to NYC & Company. They are expected to reach a maximum of 98 percent of pre-pandemic levels by 2024 (see Figure 14). The Global Business Travel Association forecasts that global business spending will return to 2019 levels ($1.43 trillion) by 2025. The recovery of corporate travel is projected to be a slow process. While worldwide business travel may rebound faster, global business metropolitan centers with high population densities such as New York City may be slower to recover.

FIGURE 14 – Leisure and Business Traveler Projections

Sources: NYC & Company; OSC analysis

According to McKinsey & Company, business travel has a higher volatility over economic cycles and is slower to recover after a downturn. After the financial crisis of 2008-09, international business travel to the nation declined by more than 13 percent, compared to 7 percent for international leisure. While leisure travel recovered within two years, business travel took five years to fully rebound.

The City must also address both the reality and perceptions of rising crime. Some crimes such as murders and shootings are higher than five years ago, but overall crime remains well below levels in the early 2000s. Furthermore, empty streets and increased public homelessness may be contributing to perceptions of a less safe City. There is a strong relationship between tourism and the perception of crime, and the City’s tourism outlook fundamentally relies on a feeling of public safety for all visitors.

Reigniting the Return

In reigniting the return for New York City’s tourism industry, policy makers, advocates and industry stakeholders must focus on vaccinations of workers and fully reopening establishments safely, but also on developing a more proactive strategy for reengaging domestic travelers and cultivating international and business travelers to help the industry reach and eventually exceed 2019 levels.

In the interim, the City and State must also leverage federal aid and continue to provide relief funding and technical assistance to individuals and businesses in the industry as it restarts. While some travel restrictions are lifting, the current expectation is that visitors will not return to pre-pandemic levels for several years. The government must provide a much-needed lifeline to sustain this vital component of New York City’s economy until visitors and their spending return.

The following recommendations expand on earlier, more targeted, recommendations for restaurants and bars, retail businesses, and arts and entertainment venues and operators, which remain necessary. The strategic response for New York City’s tourism industry should focus on:

- Building the infrastructure and systems that aid flexible adherence to health and safety guidelines by individuals and businesses, including the expansion of public space for tourism activities. Managing crime must also be a focal point for creating a welcoming environment. Public health and safety are fundamental for encouraging visitors to return to the City.

- Facilitating the acceleration of airport enhancements as well as maintaining and enhancing local transportation options, such as mass transit. Expanding capacity to take in visitors and improving mobility in the region in a sustainable fashion should alleviate the burden on arriving visitors and encourage more robust and diverse experiences.

- Investing in and promoting tourist activities, including support for agencies designed to coordinate such activities (e.g., NYC & Company). The Mayor has announced a $30 million advertising campaign to jump-start tourism beginning June 2021, using federal relief funds. While this is an important step forward, the City should consider longer-term investment for continued campaigns to target shifting markets as tourism returns. The City’s spending on these activities has lagged behind other major domestic destinations, such as Las Vegas.

- Analyzing and refining targeted relief programs, particularly for the accommodation and transportation industries, to ensure that existing and new programs reach workers and alleviate short-term pressure for operators from taxes, loan payments or related fees, so that pre-pandemic operations may return.

- Integrating new technology to extend and improve engagement with visitors and help streamline compliance with public health protocols. Efforts to provide visitors with simplified means of navigating the City and the different components of a visitor’s itinerary should improve the visitor experience, social interaction and enhance the City’s reputation and engagement with its tourists.

The challenges that face the industry are multifaceted, and historical comparisons indicate the City may be facing a slow, protracted recovery. However, the unprecedented level of relief and stimulus funding, in the United States and globally, and the innate human desire to travel and enjoy new experiences should not be underestimated. These recommendations are merely initial steps for a more comprehensive strategy to reinvigorate the tourism industry in the City that never sleeps.

1 MasterCard Global Cities Destination Index, 2019; and Congressional Research Service, U.S. Travel and Tourism: Industry Trends and Policy Issues for Congress (2015), at EveryCRSReport.com.

2 Country-specific international data is from Tourism Economics.

3 Based on Tourism Economics data from 2000 to 2020.

4 The 2019 estimate was based on Tourism Economics data for 2019, and the 2020 total was based on NYC & Company’s reported share in 2019.

5 Transient travelers are predominantly on the move and seek short-term, often urgent, overnight stays.

6 Meeting and convention travelers are part of business travel and their activities are commonly referred to as MICE: Meetings, Incentives, Conferences & Exhibitions.

7 Office of the State Comptroller, Report 4-2021, The Restaurant Industry in New York City, September 2020; Report 8-2021, The Retail Sector in New York City, December 2020; and Report 12-2021, Arts, Entertainment and Recreation in New York City, February 2021.

8 New York State Department of Labor, New York State’s Travel and Tourism Sector: A Statewide and Regional Analysis, June 2017.

9 See Report 12-2021, Arts, Entertainment and Recreation in New York City, February 2021 for further clarification.

10 Includes the following NAICS codes: 721110, 721120, 721191 and 721199. See Appendix A for details.

11 Office of the State Comptroller, Report 2-2017, The Hotel Industry in New York City, June 2016.

12 This analysis excludes workers employed by government authorities, such as the Metropolitan Transportation Authority, although part of subway ridership decline has been attributed to fewer tourists.

13 New York City Taxi and Limousine Service, Annual Reports to New York City Council, https://www1.nyc.gov/site/tlc/about/industry-reports.page.

14 For more information, see Office of the State Comptroller, Report 10-2021, The Paycheck Protection Program in New York City: What’s Next?, February 2021.

15 Indirect effects stem from business spending in the supply chain and induced effects are generated by employees’ spending within the business supply chain.

16 National data is from the International Trade Association.

17 The Department of Finance’s Tentative Property Assessment Roll for FY 2021-2022 indicates a decline in market value of 24 percent for hotels and 21 percent for retail store buildings.

APPENDIX A – OSC Tourism Industry Definition

| 2017 NAICS | Title / Description | Weight |

| 441210 | Recreational Vehicle Dealers | 100% |

| 441222 | Boat Dealers | 100% |

| 443142 | Electronics Stores | 20% |

| 445110 | Supermarkets and Other Grocery (except Convenience) Stores | 20% |

| 445120 | Convenience Stores | 20% |

| 445230 | Fruit and Vegetable Markets | 20% |

| 445291 | Baked Goods Stores | 20% |

| 445292 | Confectionery and Nut Stores | 20% |

| 445299 | All Other Specialty Food Stores | 20% |

| 445310 | Beer, Wine, and Liquor Stores | 20% |

| 446110 | Pharmacies and Drug Stores | 20% |

| 446120 | Cosmetics, Beauty Supplies, and Perfume Stores | 20% |

| 446130 | Optical Goods Stores | 20% |

| 446191 | Food (Health) Supplement Stores | 20% |

| 446199 | All Other Health and Personal Care Stores | 20% |

| 447110 | Gasoline Stations with Convenience Stores | 7% |

| 447190 | Other Gasoline Stations | 7% |

| 448110 | Men's Clothing Stores | 20% |

| 448120 | Women's Clothing Stores | 20% |

| 448130 | Children's and Infants' Clothing Stores | 20% |

| 448140 | Family Clothing Stores | 20% |

| 448150 | Clothing Accessories Stores | 20% |

| 448190 | Other Clothing Stores | 20% |

| 448210 | Shoe Stores | 20% |

| 448310 | Jewelry Stores | 20% |

| 448320 | Luggage and Leather Goods Stores | 20% |

| 451110 | Sporting Goods Stores | 20% |

| 452111 | Hobby, Toy, and Game Stores | 20% |

| 452112 | News Dealers and Newsstands | 20% |

| 452210 | Department Stores | 20% |

| 452311 | Warehouse Clubs and Supercenters | 20% |

| 452319 | All Other General Merchandise Stores | 20% |

| 453220 | Gift, Novelty, and Souvenir Stores | 75% |

| 481111 | Scheduled Passenger Air Transportation | 100% |

| 481211 | Nonscheduled Chartered Passenger Air Transportation | 100% |

| 483112 | Deep Sea Passenger Transportation | 100% |

| 483114 | Coastal and Great Lakes Passenger Transportation | 100% |

| 483212 | Inland Water Passenger Transportation | 100% |

| 485210 | Interurban and Rural Bus Transportation | 100% |

| 485310 | Taxi Service | 46% |

| 485320 | Limousine Service | 46% |

| 485510 | Charter Bus Industry | 100% |

| 485999 | All Other Transit and Ground Passenger Transportation | 100% |

| 487110 | Scenic and Sightseeing Transportation, Land | 100% |

| 487210 | Scenic and Sightseeing Transportation, Water | 100% |

| 487990 | Scenic and Sightseeing Transportation, Other | 100% |

| 488111 | Air Traffic Control | 100% |

| 488119 | Other Airport Operations | 100% |

| 488490 | Other Support Activities for Road Transportation | 100% |

| 512131 | Motion Picture Theaters (except Drive-Ins) | 10% |

| 512132 | Drive-In Motion Picture Theaters | 10% |

| 532111 | Passenger Car Rental | 80% |

| 532120 | Truck, Utility Trailer, and RV (Recreational Vehicle) Rental and Leasing | 80% |

| 561510 | Travel Agencies | 100% |

| 561520 | Tour Operators | 100% |

| 561591 | Convention and Visitors Bureaus | 100% |

| 561599 | All Other Travel Arrangement and Reservation Services | 100% |

| 711110 | Theater Companies and Dinner Theaters | 30% |

| 711120 | Dance Companies | 30% |

| 711130 | Musical Groups and Artists | 30% |

| 711190 | Other Performing Arts Companies | 30% |

| 711211 | Sports Teams and Clubs | 30% |

| 711212 | Racetracks | 30% |

| 711219 | Other Spectator Sports | 30% |

| 711310 | Promoters of Performing Arts, Sports, and Similar Events with Facilities | 100% |

| 711320 | Promoters of Performing Arts, Sports, and Similar Events without Facilities | 100% |

| 711410 | Agents and Managers for Artists, Athletes, Entertainers, and Other Public Figures | 100% |

| 711510 | Independent Artists, Writers, and Performers | 100% |

| 712110 | Museums | 100% |

| 712120 | Historical Sites | 100% |

| 712130 | Zoos and Botanical Gardens | 100% |

| 712190 | Nature Parks and Other Similar Institutions | 100% |

| 713110 | Amusement and Theme Parks | 100% |

| 713120 | Amusement Arcades | 100% |

| 713210 | Casinos (except Casino Hotels) | 75% |

| 713290 | Other Gambling Industries | 75% |

| 713910 | Golf Courses and Country Clubs | 25% |

| 713920 | Skiing Facilities | 100% |

| 713930 | Marinas | 75% |

| 713940 | Fitness and Recreational Sports Centers | 10% |

| 713950 | Bowling Centers | 10% |

| 713990 | All Other Amusement and Recreation Industries | 50% |

| 721110 | Hotels (except Casino Hotels) and Motels | 100% |

| 721120 | Casino Hotels | 100% |

| 721191 | Bed-and-Breakfast Inns | 100% |

| 721199 | All Other Traveler Accommodation | 100% |

| 721211 | RV (Recreational Vehicle) Parks and Campgrounds | 100% |

| 721214 | Recreational and Vacation Camps (except Campgrounds) | 100% |

| 721310 | Rooming and Boarding Houses | 50% |

| 722310 | Food Service Contractors | 20% |

| 722320 | Caterers | 10% |

| 722330 | Mobile Food Services | 20% |

| 722410 | Drinking Places (Alcoholic Beverages) | 20% |

| 722511 | Full-Service Restaurants | 20% |

| 722513 | Limited-Service Restaurants | 20% |

| 722514 | Cafeterias, Grill Buffets, and Buffets | 20% |

| 722515 | Snack and Nonalcoholic Beverage Bars | 20% |

| 812111 | Barber Shops | 10% |

| 812112 | Beauty Salons | 10% |

| 812113 | Manicure and Pedicure Salons | 10% |

| 812199 | Other Personal Care Services | 10% |

| 812320 | Dry Cleaning and Laundry Services (except Coin-Operated) | 10% |

Appendix A lists the North American Industry Classification System (NAICS) sectors used in OSC’s tourism industry definition and their respective weighting. This definition builds on prior analysis from the New York State Department of Labor (New York State’s Travel and Tourism Sector: A Statewide and Regional Analysis, June 2017).

NAICS Used for Years Prior to 2007

| 2017 NAICS | Title / Description | Weight |

| 443112 | Radio, Television, and Other Electronic Stores | 20% |

| 443120 | Computer and Software Stores | 20% |

| 443130 | Camera and Photographic Supply Stores | 20% |

| 452910 | Warehouse Clubs and Supercenters | 20% |

| 452990 | All Other General Merchandise Stores | 20% |

| 722110 | Full-Service Restaurants | 20% |

| 722211 | Limited-Service Restaurants | 20% |

| 722212 | Cafeterias, Grill Buffets, and Buffets | 20% |

| 722213 | Snack and Nonalcoholic Beverage Bars | 20% |